Learn how to backtesting trading strategies correctly using a structured trading journal. Avoid common mistakes and validate your edge with data.

Table of Contents

- 1 What Is Backtesting Trading Strategies?

- 2 Key Backtesting Methods

- 3 How to Backtest Trading Strategies Step by Step

- 4 Essential Backtest Metrics You Must Track (and Why)

- 5 Common Backtesting Mistakes (and How to Avoid Them)

- 6 Software Tools for Backtesting Trading Strategies (2026)

- 7 Build confidence before trading real money.

What Is Backtesting Trading Strategies?

Backtesting trading strategies is the process of applying a defined trading system to historical market data to evaluate its performance.

A proper backtest answers questions like:

- Is this strategy profitable over a meaningful sample size?

- What is the win rate and average RR?

- In which sessions or timeframes does it perform best?

- Which setups should be removed or refined?

Without structure, backtesting becomes unreliable.

Key Backtesting Methods

Manual Backtesting

Manual backtesting involves moving candle-by-candle through historical charts and simulating trades as if they were live.

Pros:

- Builds market understanding

- Ideal for discretionary strategies

Cons:

- Time-consuming

- Requires strict discipline and logging

Automated Backtesting

Automated backtesting uses scripts or algorithms to test strategies over years of data instantly.

Pros:

- Fast

- Deep statistical analysis

Cons:

- Requires coding

- Less suitable for discretionary decision-making

Most discretionary traders benefit from manual backtesting with a structured journal.

How to Backtest Trading Strategies Step by Step

Step 1: Define One Strategy = One Variable

Each strategy or setup must be tested independently.

Changing rules mid-test invalidates your results.

Define clearly:

- Entry conditions

- Stop-loss logic

- Take-profit rules

- Session and timeframe

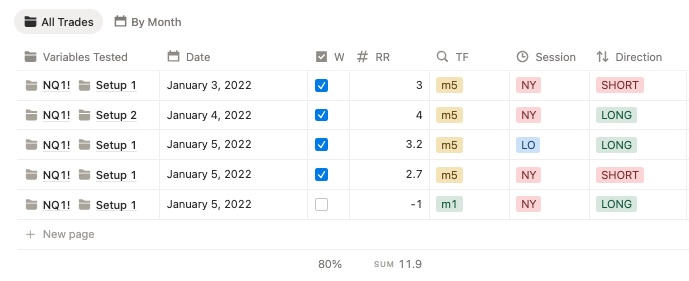

Step 2: Log Every Backtested Trade Consistently

Each trade should be recorded with the same structure:

- Date

- Session (NY, London, etc.)

- Timeframe

- Trade direction (Long / Short)

- Risk-Reward (RR)

- Win or loss outcome

- Notes and context

Consistency matters more than speed.

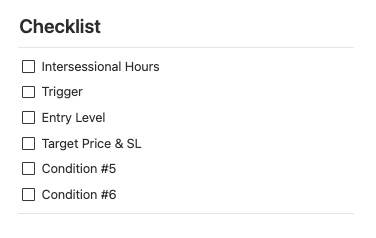

Step 3: Validate Trades Using a Checklist

Many traders unknowingly include invalid trades in their backtests.

A checklist helps you:

- Confirm the trade followed all rules

- Eliminate “almost valid” setups

- Keep your data clean

Only validated trades should count toward performance metrics.

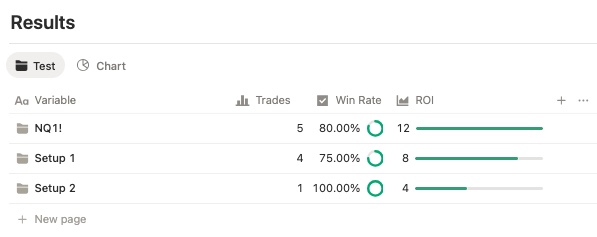

Step 4: Analyze Results by Setup or Condition

After a meaningful sample size (30+ trades minimum), analyze:

- Win rate per setup

- ROI per variable

- Performance by session or timeframe

This allows you to objectively compare strategies instead of relying on memory or intuition.

Step 5: Refine, Retest, or Discard

Backtesting trading strategies is an iterative process.

Based on results:

- Refine entry or exit rules

- Limit the strategy to specific conditions

- Discard setups with poor expectancy

Only validated strategies should move to demo or live trading.

Essential Backtest Metrics You Must Track (and Why)

Win Rate

Useful, but meaningless without RR.

Risk-Reward Ratio (RR)

Defines expectancy. A low win rate can still be profitable with high RR.

Drawdown

Shows the psychological and financial stress of the strategy.

ROI / Net Return

Helps compare setups objectively.

Good backtesting focuses on expectancy, not just winners.

Common Backtesting Mistakes (and How to Avoid Them)

- Overfitting: Optimizing too closely to past data

- Ignoring transaction costs: Spreads and commissions matter

- Lookahead bias: Using information not available at the time

- Small sample sizes: Less than 30 trades is noise

- Rule changes mid-test: Invalidates results

A structured workflow minimizes these errors.

Software Tools for Backtesting Trading Strategies (2026)

Commonly used tools include:

- TradingView (manual bar replay)

- FX Replay

- MetaTrader 4 / 5

- Excel or spreadsheets

- Notion trading backtesting journal template

Each tool serves a different role in the backtesting process.

Build confidence before trading real money.

Start using a professional Trading Backtesting Journal and validate your trading strategies with data.